Retails goods are frequently sold with a warranty (or guarantee) that they will operate satisfactorily for a specified period of time. The accounting treatment depends on:

- Whether customers have an option to purchase the warranty separately, and

- Whether the warranty is part of the overall package of goods sold to the customer, and if so, whether the warranty simply provides assurance that the goods are in compliance with the agreed upon specifications in the contract.

Agreed upon specifications often relate to an assurance that an item will function properly for a specified period, and may link to legal requirements in some jurisdictions.

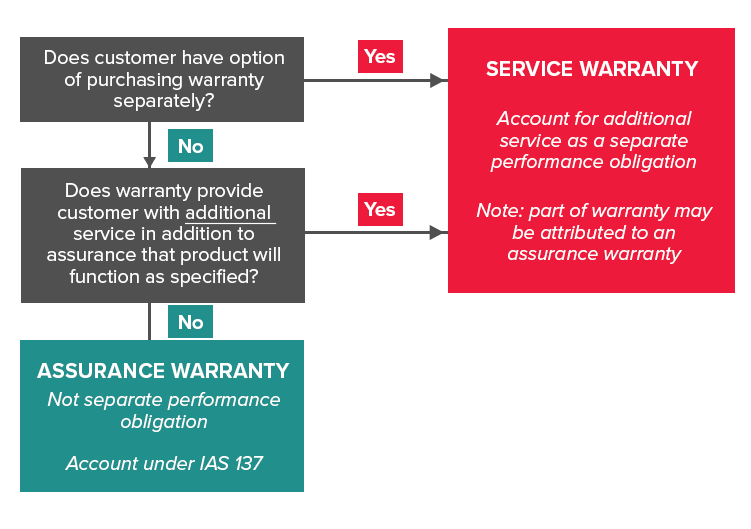

If customers have an option to purchase a warranty separately from the goods themselves, this is accounted for separately. If the warranty is part of the overall package, if it simply provides an assurance of compliance with agreed upon specifications, it is not accounted for separately. If it goes beyond compliance with agreed upon specifications, then it is accounted for separately, regardless of whether it is identified as a separate component of the sales transaction.

Goods may also be sold with a warranty for a specified period (such as 12 months), with the customer being given the right to renew the warranty for a further 12 months at a discount from the standard selling price. In these cases, the consideration received for the first 12-month warranty may need to be split between the initial 12-month licence and the renewal right, with revenue relating to that renewal right being deferred and recognised in a future period.

It is common practice to offer customers ‘free’ or extended warranties as an inducement to encourage purchase.

The key to determining whether this warranty is a separate performance obligation under IFRS 15 is to determine whether the warranties are ‘assurance-type’ warranties (which are usually required by law) or are warranties that can be sold separately. There is no change to accounting for ‘assurance-type’ warranties (which are not a separate performance obligation as all they do is satisfy that the good sold is correctly functioning). However, extended warranties that can be sold separately are required to be accounted for separately which will result in delayed revenue.

The following decision tree could be used to determine whether a warranty is an ‘assurance warranty’ or a ‘service warranty’, as well as the appropriate accounting treatment:

Example – Assurance type warranties

Question

Manufacturer A sells laptop computers with a 12-month warranty which assures that the laptops will work as intended for 12 months. The warranty is not sold separately. How should Manufacturer A account for the warranty?

Answer

Because the warranty provides the customer with the assurance that the laptop will work as intended for one year, Manufacturer A will account for this ‘assurance-type’ warranty in accordance with IAS 37 Provisions, Contingent Liabilities and Contingent Assets, i.e. a provision is raised for the expected cost of repairing the product in the next 12 months. Assurance-type warranties do not result in a change to current practice re the recognition of revenue, i.e. this does not represent a separate performance obligation.

Example – Providing a free extended warranty

Question

On 29 June 2018, Retailer C is running a special promotion on its washing machines. The selling price of the washing machine is $1,000. Customers will receive a free 24-month extended warranty, in addition to the 12-month standard warranty. The same 24-month extended warranty can be purchased from the manufacturer for $200. How should Retailer C account for the sale? Assume that the standalone selling price of the washing machine is $1,000.

Answer

A portion of the selling price needs to be allocated to the extended warranty based on the relative standalone selling price.

| Contract components | Standalone selling price | Revenue |

| Washing machine | $1,000 | $833 ($1,000x($1,000/$1,200)) |

| Extended warranty | $200 | $167 ($1,000x($200/$1,200)) |

| $1,200 | $1,000 |

Retailer C will recognise $833 when the washing machine is sold. $167 is deferred until the warranty obligation is satisfied.

The common practice today is to recognise $1,000 as revenue, and a provision under IAS 37.

| 30 June 2018 | 30 June 2019 | 30 June 2020 | Total | |

| IFRS 15 | ||||

| Washing machine | $833 | - | - | $833 |

| 2 year extended warranty | $84 | $84 | $167 | |

| Total | $833 | $84 | $84 | $1,000 |

| IAS 18 | ||||

| Washing machine | $1,000 | - | - | $1,000 |

Practical implications on systems and processes

Some of the practical implications on systems and processes for Retailer C include:

- Processes to identify that there are two performance obligations

- Working out the standalone selling price of the extended warranty. Use one of the following methods to determine standalone selling prices:

- How much competitors are selling the service for

- Estimate the price customers would be willing to pay

- Use an expected cost + appropriate margin approach

- System to be able to split revenue at point of sale

- Systems to apportion and defer revenue.

Subscribe to receive the latest BDO News and Insights

Please fill out the following form to access the download.